- Be a Kenyan over 18 years old and in gainful employment

- Be of a good moral character and sound mind

- Pay registration fee of Kshs 10,000

- Buy a minimum of 5 Investment capital shares worth a total of Kshs 50,000

- Maintain monthly minimum Savings contributions of Kshs 10,000.

- SACCOs have lower interest rates compared with commercial banks.

- As a member of the SACCO, you earn interest on your savings which are part of what you have borrowed lowering your borrowing costs further.

- While repaying a SACCO loan, a member is expected to still maintain the same level of monthly savings as they did before. This builds a saving discipline, and helps one accumulate a substantial savings base

Yes. As long as long as there is no conflict of interest with Stoke UK Diaspora Sacco.

The Sacco primarily invests in Real Estate including land and housing properties through our Sacco Investment arm ( PLC) . Short term investments include Money markets, fixed term and government securities.

SACCOs are governed by the SACCO bylaws which state the objectives, membership, share capital, organizational structure, management and lending regulations. Sacco affairs are managed and governed by the Cooperative Society Act.

Yes. With the approval of the Committee, a member may at any time transfer shares to another member but not to any other person. Such transfers must be in writing and at nominal value. All transfers of shares shall be registered with the society and no transfer shall be valid unless so registered. A fee of Kshs 1,000 shall be payable by the transferee.

A sum of money paid regularly (typically annually) by the Sacco to its shareholders out of its profits.

Shares earn dividends annually based on the profits accrued from Sacco investments. Dividends are allocated based on the number of capital shares owned by each member.

Interest is computed based on weighted average method. The interest payable to the member is dependent on the income the society makes as at the end of every financial year.

Share capital is the permanent member contribution toward the Sacco capital and forms part of Sacco equity. Shares cannot be withdrawn even on exit from the Sacco but can be transferred to another willing member.

It is expected that members will buy the minimum 5 shares within 6 months of joining. Members can also regularly buy as many shares as they can as long as it’s not more than one fifth of the society’s shares.

No, shares do not count towards the loan but any shares above the minimum share capital of 50,000 can be used as security.

Should a member wish to withdraw from the Sacco the exit procedure is as below:

- Fill the Membership exit form

- The member will be required to give the Sacco 60 days notice

- Deposits refunded less any monies and loans owed to the society and its affiliated partners

- If you have guaranteed any active loans, the creditor will need to find an alternative guarantor replacement

- Member may opt to retain shares or sell/transfer to an existing member

Yes, as long as you continue to make contributions into your savings account and continue making the payments towards your loan if any.

As a member of the SACCO, the loan amount depends on the loan product.

You can borrow a loan after the required 6 months of regular contribution to your Main Savings Account without any arrears or late payments.

A member can borrow up to 70% of their savings without needing an extra security.

The following are admissible securities for loans:

- The savings of a member

- The shares of a member above the minimum share capital of Kshs 50,000

- The shares and savings of guarantor(s),

- Title deed

- Debenture on stock or securities.

NOTE:

The committee shall not accept as guarantor, a member who has taken a loan and has already guaranteed three loans.

No member of the Management and Supervisory shall act as guarantor

Yes, you can repay earlier. No interest or penalty is charged for clearing a loan earlier than the contracted period. The interest to pay will be lower because the interest is based on reducing balance.

We take great care in how we handle members money:

- Credible Banks: Currently, Stoke UK Diaspora Sacco banks with Cooperative bank and KCB bank which are both governed by the banking laws under the Central Bank.

- Three Account Signatories: Stoke UK Diaspora Sacco is member owned. Members deposit their funds directly into Sacco Bank accounts. No money gets in the hands of the board members or any other person. The Sacco has 3 signatories to the bank accounts: The Chairman, the Treasurer and the Secretary ALL three MUST sign every transaction. One of our core values is INTEGRITY which we uphold steadfastly.

- Transparency in business deals: Stoke UK Diaspora Sacco is member driven meaning that members decide on when, where and how to invest. The Management Committee and various subcommittees are there to support the operations of the Sacco by conducting due diligence. We are guided by core values of Integrity, professionalism and transparency.

- Loans management: The Savings and Credit subcommittee is composed entirely of non-executive members to ensure equitable awarding of loans. Any loans taken by members must be secured by either shares or other collateral subject to approval by the credit control committee. In the unlikely event that the Sacco goes bankrupt, the society shall be dissolved in accordance with the procedures set forth in the Act and Rules.

In the unlikely event that the Sacco goes bankrupt, the society shall be dissolved in accordance with the procedures set forth in the Act and Rules.

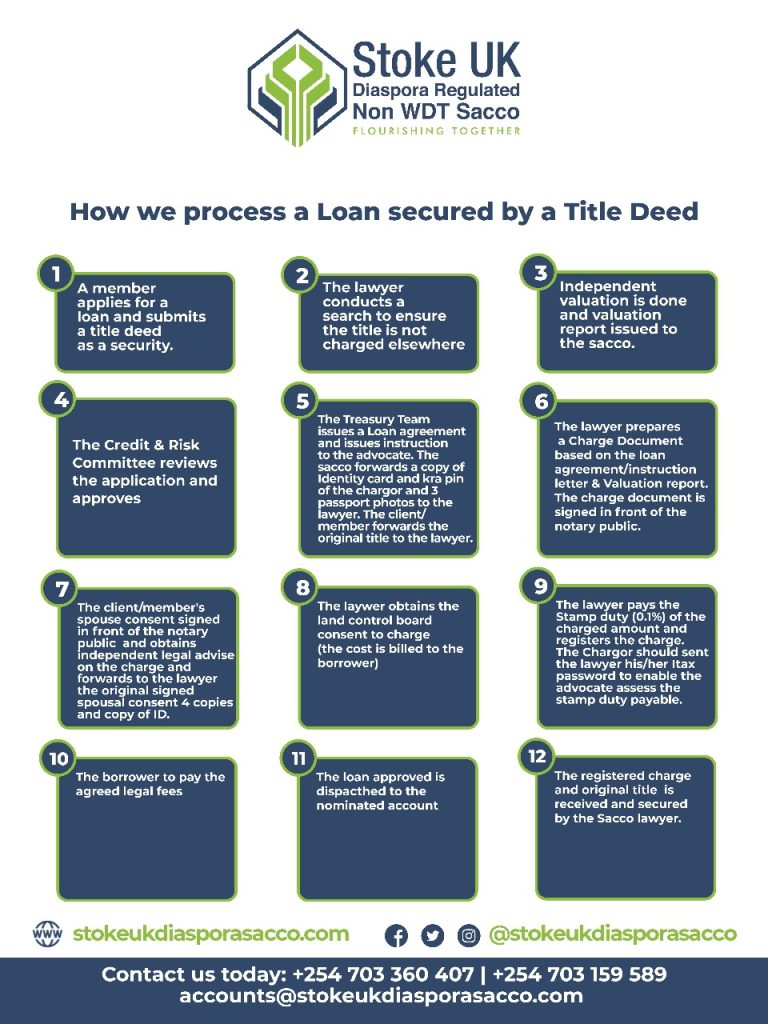

The details below illustrates how a title deed can be used to secure a loan from the SACCO.

You can make Sacco contribution using the below channels:

You can access the member account by visiting https://portal.stokeukdiasporasacco.com/ or download our app on the Apple App Store or Google Play Store today!